Global Traffic Grows, but Airlines Face Missed Opportunities Amid Manufacturer Delays

Global air traffic saw significant growth in November, but airlines face challenges due to manufacturer delays in delivering aircraft, limiting their ability to meet demand, modernize fleets, and improve services.

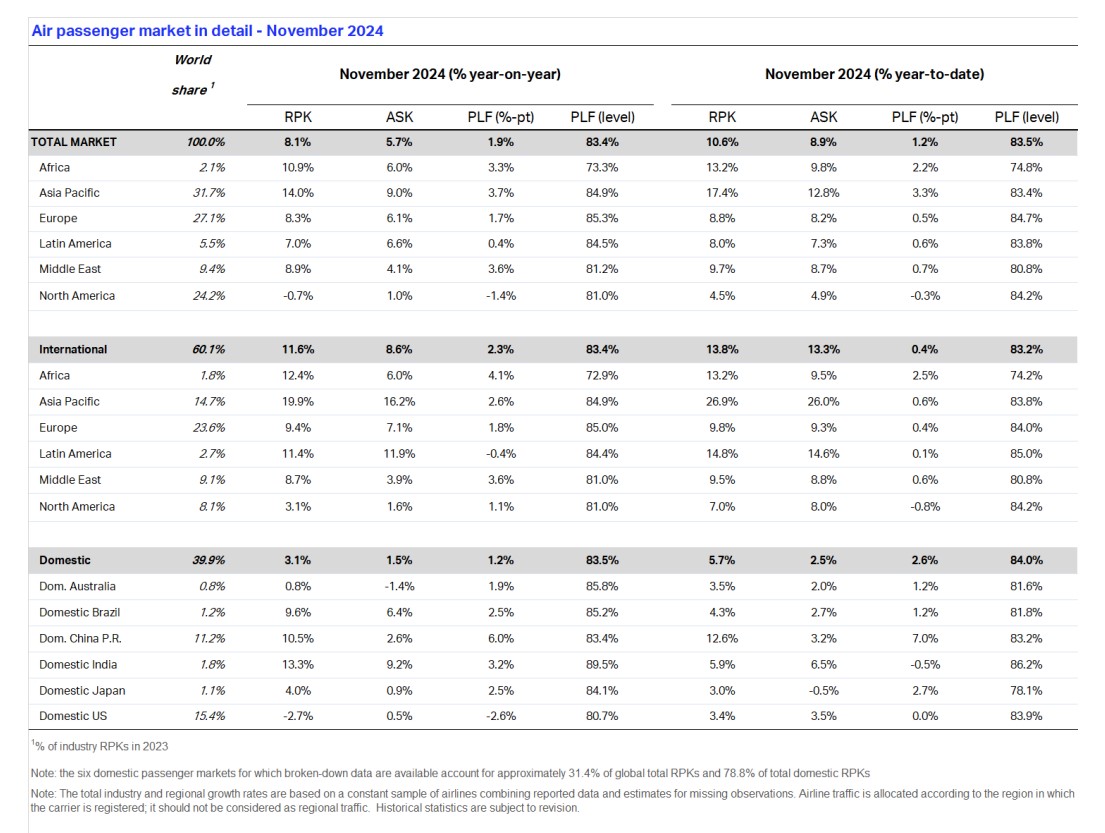

The International Air Transport Association (IATA) reported an 8.1% year-on-year increase in global passenger demand, measured in revenue passenger kilometers (RPK), for November 2024. Capacity, assessed in available seat kilometers (ASK), grew by 5.7%, while the load factor reached 83.4%, a record high for the month of November and 1.9 percentage points above the same month in 2023.

The organization highlighted that international passenger demand rose by 11.6%, with capacity increasing by 8.6%. European carriers achieved the highest load factor (85%), while Asia-Pacific airlines recorded the largest demand growth at 19.9%.

Domestic markets saw a 3.1% increase in RPK compared to November 2023, while capacity grew by 1.5%. This resulted in a load factor of 83.5%, up 1.2 percentage points. However, the U.S. domestic market contracted by 2.7%, continuing a downward trend since June 2024. This decline is attributed to reduced activity by low-cost carriers, while mainline operators experienced growth.

“November was another month of strong growth in the demand for air travel with an overall expansion of 8.1%. The month was also another reminder of the supply chain issues that are preventing airlines from getting the aircraft they need to meet growing demand. Capacity growth is lagging demand by 2.4 ppts and load factors are at record levels," said Willie Walsh, IATA’s Director General.

“Airlines are missing out on opportunities to better serve customers, modernize their products and improve their environmental performance because aircraft are not being delivered on time. The 2025 New Year’s resolution for the aerospace manufacturing sector must be finding a fast and durable solution for their supply chain issues,” he added.

Regional Performance

Asia-Pacific airlines led the global growth with a 14% increase in RPK, supported by a 9% capacity expansion and a load factor of 84.9%. This region also demonstrated robust international growth of 19.9%, with capacity rising by 16.2% and a load factor increase of 2.6 percentage points.

European airlines recorded an 8.3% increase in overall demand, accompanied by a 6.1% rise in capacity. The load factor reached 85.3%, underscoring the region’s high efficiency in matching supply with demand.

African carriers experienced a 10.9% rise in RPK, with a 6% increase in capacity. The load factor improved by 4.1 percentage points to 73.3%, showing significant progress in regional connectivity.

In the Middle East, demand grew by 8.9%, while capacity expanded by 4.1%. The load factor reached 81.2%, marking a 3.6 percentage point improvement compared to November 2023.

Latin American airlines achieved a 7% increase in RPK, with capacity growing by 6.6%. The load factor stood at 84.5%, reflecting strong demand across the region.

North America reported a 0.7% decline in total demand, with capacity increasing by 1%. The load factor fell slightly to 81%, highlighting the ongoing challenges in the U.S. domestic market.

Domestic Market Highlights

India led domestic market growth with a 13.3% increase in RPK and the highest load factor among analyzed markets at 89.5%. China followed with a 10.5% rise in demand and a capacity increase of 2.6%. Brazil also demonstrated strong growth, with a 9.6% rise in RPK and a load factor of 85.2%.

According to IATA, the global aviation market continues its steady recovery, driven by increased international demand. However, the association emphasized the need for improved supply chain efficiencies to support airlines in meeting rising passenger numbers and modernizing fleets.

See full report: IATA Passenger Market Analysis - Novembrer 2024

AUTOR

Contando la aviación desde marzo del año 2000. Fundador y Managing Editor de Aviacionline. Base: ROS Origen: RES

Comentarios

Para comentar, debés estar registrado

Por favor, iniciá sesión